Talking about money with your romantic partner or spouse can be tough — especially when you don’t understand or know much about how they think about money.

Thank you for reading this post, don't forget to subscribe!A new survey finds that 64% of couples admit to being “financially incompatible” with their partners, with different philosophies about spending, saving, and investing their money.

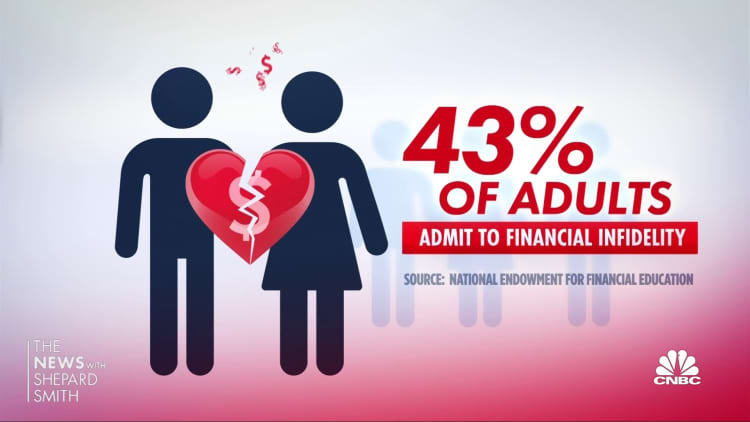

Unfortunately, this friction can lead some to commit so-called financial infidelity, hiding purchases from their partner. In this survey by the fintech firm Bread Financial, 45% of coupled adults admitted they’re guilty.

Even if there is no financial cheating, money issues can still cause strain in relationships, arguments or even divorce. One in 5 couples identifies money as their greatest relationship challenge, according to the most recent Couples & Money survey by Fidelity Investments.

More from Personal Finance:

5 money moves can set you up for financial success in 2023

These strategies can help you dig out of holiday debt

Nonprofit stresses education to change face of angel investing

Many financial advisors recommend communicating about how each of you handles your finances to figure out your partner’s “money mindset.” It’s part of the work you need to do to help build a stronger relationship, financial psychologists say. Having that “money talk” is more important than whether you merge your accounts or go with the “yours, mine, ours” approach.

So how do you start what can be a difficult conversation? Here are some tips about delving into the “money talk” no matter what stage of the relationship you’re in.

If you’re newly partnered or married

Jeong Hoon Choi / Eyeem | Eyeem | Getty Images

Gen Z and millennials may argue with their partner over finances more than older couples. Millennials may also talk more frequently about money than baby boomer couples. But if you’ve just coupled, what’s that icebreaker?

Start with a simple question about how your partner handled their finances before you got together. A simple question like whether they’re taking advantage of their 401(k) or 403(b) retirement plan at work can tell you a lot about their planning, said Lawrence Sprung, a certified financial planner and founder and wealth advisor at Mitlin Financial in Hauppauge, New York. Then do this:

- Open the books: Show one another your financial information. This “show and tell” can be a way to talk about how much student loan or credit card debt you have or how you intend to save for retirement.

- Set a time and place for a special date: Pick a day and location that’s most convenient and calm for both of you for the money talk. You want to be able to focus and not be interrupted.

- Align your finances: Figure out who will handle certain money matters or how you’ll split these expenses. Make sure you both have access to shared accounts. Then decide who will pay which bills or if you’ll pay for them from a joint account.

For those married for several years

Luminola | E+ | Getty Images

Among women, more than 20% of marriages that end in divorce last about 10 years, according to the U.S. Census Bureau. Part of the reason those relationships end may be due to a lack of communication on many fronts. “Money dates” may become less frequent as other priorities take over, such as moving into a new home, starting a family, changing jobs. Still, it’s important to keep talking:

- Review your household budget: Set aside time to review your total financial picture at least once a year. Going over the year-end credit card, savings, investment, and retirement account statements can be a good place to start to see where you stand.

- Maximize your resources: You want to make the most of your combined income. Whether your merge accounts or not, you’ll need to figure out how to build your savings, while affording your necessary and discretionary expenses. Pay yourselves first by making regular savings account contributions to build an emergency fund and putting part of your pay in a retirement plan for the future.

- Then, “outline what your shared expenses are, what they cost, and how much each partner will contribute to the expenses,” said Dr. Megan Ford, a financial therapist based in Athens, Georgia. “This isn’t always an easy 50/50 split when incomes are uneven” — or if one of you is out of work right now. That’s why stashing cash in an emergency fund while working is essential.

If you’re an older couple near or in retirement

Many older couples say thinking about saving enough for retirement and making enough money for the life they want are two issues that keep them up most at night. You’ll likely sleep more soundly if you do this:

- Get on the same page about your future: The Fidelity study found 48% of couples disagree about what age they play to retire, and 52% disagree about how much should be saved by that time. Consider you may live well into your 80s or longer. Plan for how much money you will need for future goals and make sure it will be enough to last.

- Focus on managing debt: While shopping and spending may cause the biggest rift in relationships, the second most common contentious financial matter for boomers is credit card debt, according to Bread Financial’s survey. It’s time for both of you to review those annual statements again to see how much debt you are in.

- Talk to a financial professional: Having both of your speak to a financial advisor can help you continue to focus on your future, develop a financial plan and build a financial team to help. The earlier you speak with a financial professional, the better.

All couples need to plan ahead for ‘what if’

One of the most important conversations couples can have about their finances — no matter how old they are — is the one about who will make decisions for them if they get ill or are injured and can’t make them for themselves. At the same, it’s important to discuss the financial legacy you’d like to leave your partner and/or loved ones. All of that is essential to estate planning.

- Make sure you have critical estate-planning documents: In addition to your will or trust, you should have a health-care proxy, living will or advanced medical directive, and durable power of attorney.

- Review beneficiaries on your retirement and life insurance plans: Make sure they reflect the person that you want to be named, especially for same-sex couples or if you’re on a second marriage or are now uncoupled after a divorce or death of your partner.

SIGN UP: Money 101 is an 8-week learning course to financial freedom, delivered weekly to your inbox. For the Spanish version Dinero 101, click here.